Mobiles may yet restart growth at nvidia. Still, hard to complain about 50% margins.

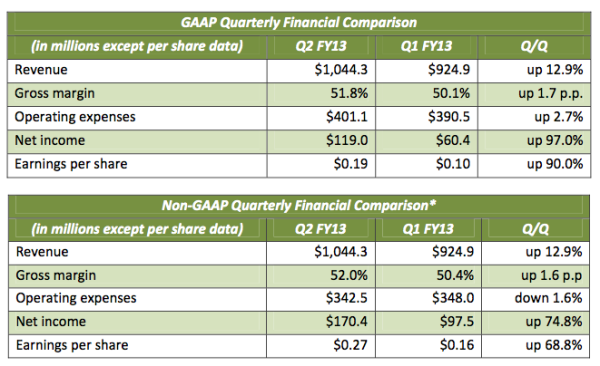

I don't normally comment on earning's calls, but this is something I've been talking a lot about in meetings offline so I decided to write up a short post. Yesterday NVIDIA announced its Q2 earnings. In short, they were good. Total revenue was up to $1.04 billion and gross margins were healthy at 51.8%. The more interesting numbers were in the breakdown of where all of that revenue came from. NVIDIA reports on revenue from three primary businesses: GPU, Professional Solutions and Consumer Products. The GPU business includes all consumer GPUs (notebook, desktop and memory - NVIDIA sells GPU + memory bundles to its partners) as well as license revenue from NVIDIA's cross licensing agreement with Intel. The Professional Solutions business is all things Quadro and Tesla. Finally the Consumer Products business is home to Tegra, Icera, game console revenue and embedded products.

I don't normally comment on earning's calls, but this is something I've been talking a lot about in meetings offline so I decided to write up a short post. Yesterday NVIDIA announced its Q2 earnings. In short, they were good. Total revenue was up to $1.04 billion and gross margins were healthy at 51.8%. The more interesting numbers were in the breakdown of where all of that revenue came from. NVIDIA reports on revenue from three primary businesses: GPU, Professional Solutions and Consumer Products. The GPU business includes all consumer GPUs (notebook, desktop and memory - NVIDIA sells GPU + memory bundles to its partners) as well as license revenue from NVIDIA's cross licensing agreement with Intel. The Professional Solutions business is all things Quadro and Tesla. Finally the Consumer Products business is home to Tegra, Icera, game console revenue and embedded products.

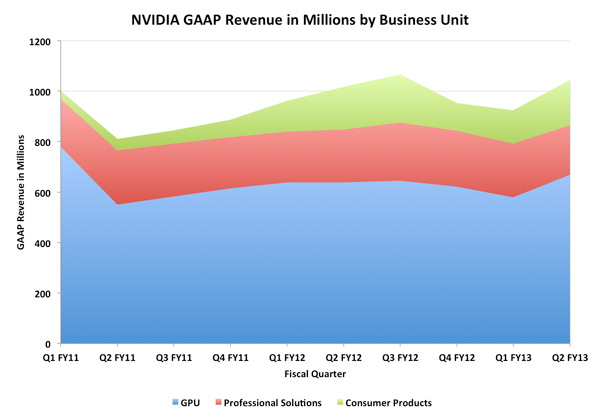

I plotted revenue across all three businesses going back over the past 2.5 years:

The quarter that just ended was NVIDIA's second quarter for fiscal year 2013 which is why the quarter stamps along the x-axis look a bit forward looking at first glance. Going back two years ago, the consumer products business was virtually nonexistent. Two years ago NVIDIA's consumer products sales were one quarter what they are today. The growth in the Tegra space has been steady since then, but late last year it saw a bit of a fall off (Tegra 2 wasn't exactly competitive in the second half of 2011). NVIDIA boasted healthy growth this quarter thanks to some fairly high profile Tegra 3 design wins, but the overall revenue for the consumer products group is still below its $191.1M peak three quarters ago. There's still a lot of hope for the business and it's definitely healthier than it was a couple of years ago, but there's still a long way to go. Ultimately NVIDIA needs to produce designs competitive enough to last until the next design cycle, and not taper off early. Tegra 2 was late to market and thus its competitive position was understandable at the end of 2011. Tegra 3 did a lot better but the real hope is for its Cortex A15 based successor, Wayne.

The quarter that just ended was NVIDIA's second quarter for fiscal year 2013 which is why the quarter stamps along the x-axis look a bit forward looking at first glance. Going back two years ago, the consumer products business was virtually nonexistent. Two years ago NVIDIA's consumer products sales were one quarter what they are today. The growth in the Tegra space has been steady since then, but late last year it saw a bit of a fall off (Tegra 2 wasn't exactly competitive in the second half of 2011). NVIDIA boasted healthy growth this quarter thanks to some fairly high profile Tegra 3 design wins, but the overall revenue for the consumer products group is still below its $191.1M peak three quarters ago. There's still a lot of hope for the business and it's definitely healthier than it was a couple of years ago, but there's still a long way to go. Ultimately NVIDIA needs to produce designs competitive enough to last until the next design cycle, and not taper off early. Tegra 2 was late to market and thus its competitive position was understandable at the end of 2011. Tegra 3 did a lot better but the real hope is for its Cortex A15 based successor, Wayne.

As it stands, Tegra (and the rest of the consumer products group) is responsible for 17.2% of NVIDIA's total quart...

NVIDIA Q2 FY13 Earnings Report: $1.04B Revenue, Tegra Sales Recover

I plotted revenue across all three businesses going back over the past 2.5 years:

As it stands, Tegra (and the rest of the consumer products group) is responsible for 17.2% of NVIDIA's total quart...